Join one of the fastest growing real estate teams in the US and Canada. Fill out the form below and we will contact you with more info.

Request property marketing plan

You're one step away from getting a free marketing plan that shows how we'll sell your home for the most amount of money in the least amount of time - hassle free.

Nick Good with eXp Realty is not an affiliate of

Envoy Mortgage Ltd. Nick Good with eXp Realty does not endorse any mortgage lender and

encourages all consumers to shop for services when looking for a mortgage loan.

The closing

costs credit offer is for up to $1000 lender credit to any applicant for loans of $150K or more

towards third-party costs provided you fund your mortgage with the BKCO Loan Team at Envoy Mortgage

Ltd. The waived fee credit will be given in the form of a lender credit at closing up to $1495. All

applications are subject to credit approval. Program terms and conditions are subject to change

without notice. Some products may not be available in all states. Reverse Mortgages will be brokered

to a third-party lender. By refinancing the existing loan, the total finance charges may be higher

over the life of the loan. Other restrictions and limitations may apply. This is not a commitment to

lend - Envoy Mortgage Ltd. #6666 (www.nmlsconsumeraccess.org) 10496 Katy Freeway, Suite 250, Houston, TX

77043, 877-232-2461 - www.envoymortgage.com | Other authorized trade names: Envoy Mortgage LP;

Envoy Mortgage of Wisconsin; Envoy Mortgage, A Limited Partnership; Envoy Mortgage, L.P.; Envoy

Mortgage, Limited Partnership; Envoy Mortgage, LP; Envoy Mortgage, LTD Limited Partnership; ENVOY

MORTGAGE, LTD, LP (USED IN VA BY: ENVOY MORTGAGE, LTD); Envoy Mortgage, LTD. (LP) | For additional

licensing information please visit https://www.envoymortgage.com/licensing-legal-information/

Let’s find you the right mortgage loan

Start The Process

We’ll help you find a local loan originator to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

Let’s find you the right mortgage loan

Start The Process

We’ll help you find a local loan originator to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

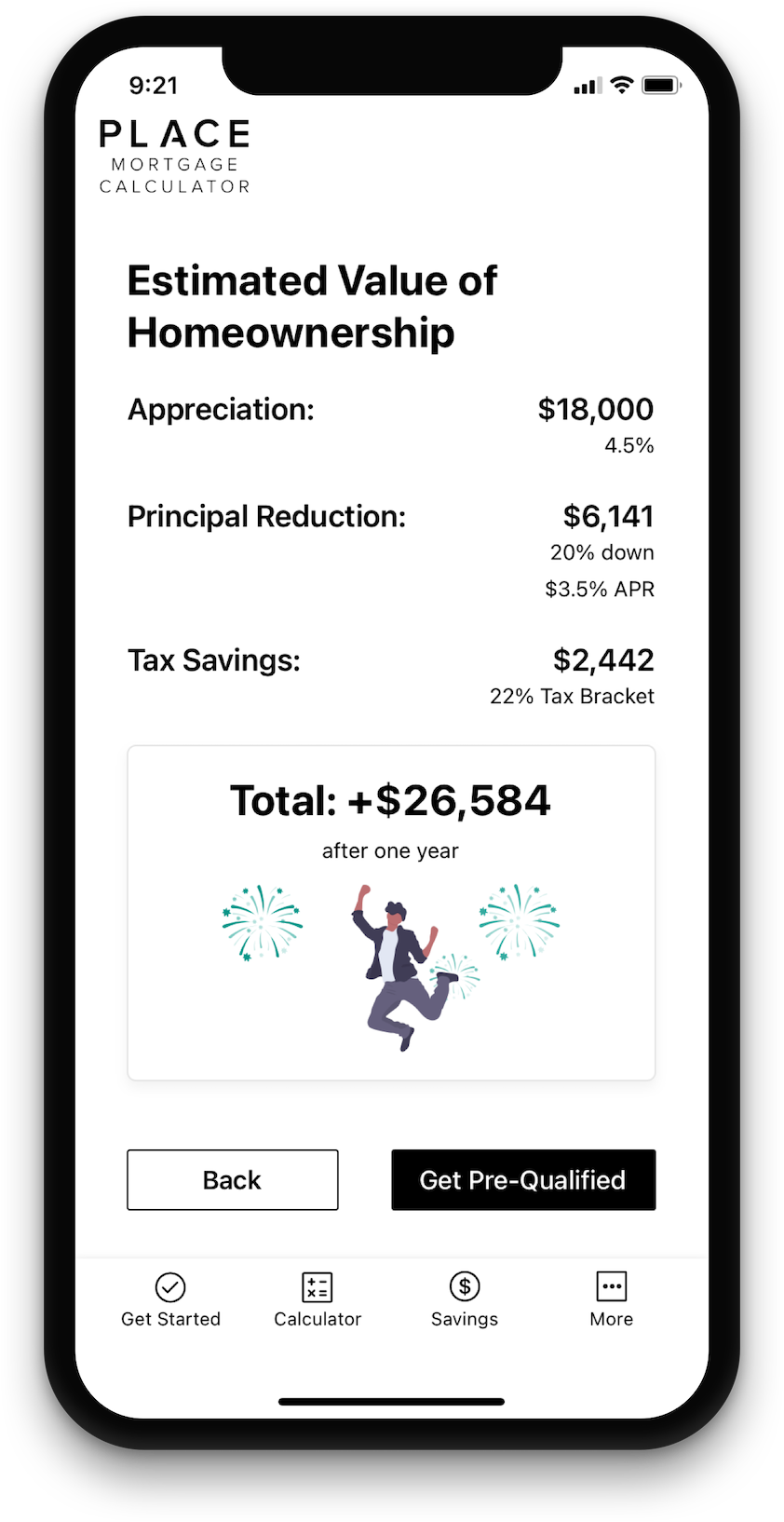

ESTIMATE YOUR MONTHLY PAYMENT

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

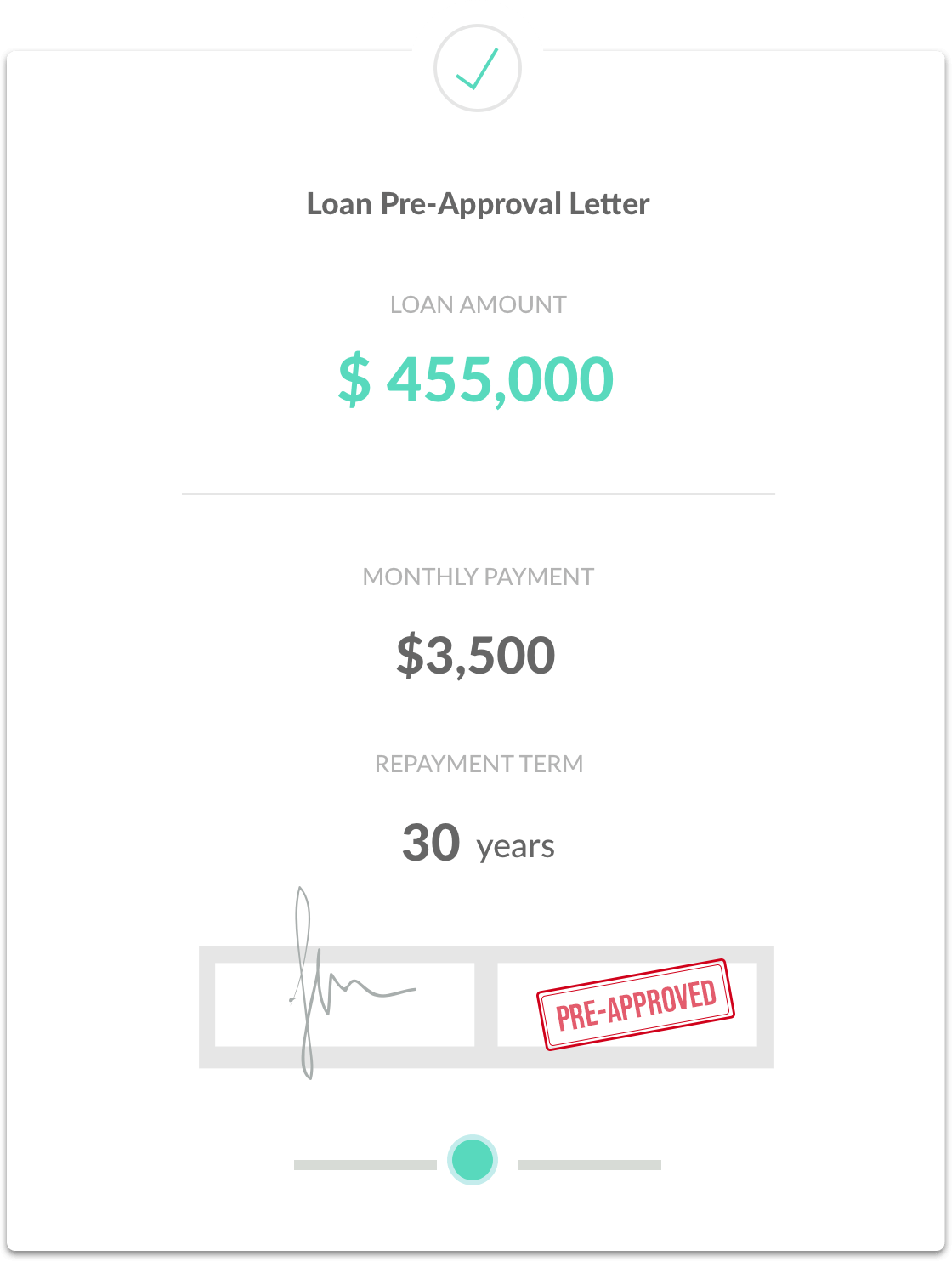

Before you start looking for a home to buy, it’s a good idea to meet with your loan originator to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets, and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns, and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment

options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an

underwriter, who reviews and approves the entire loan if it meets compliance.

What Are Closing Costs?

You've found your dream home, the seller has accepted your offer, your loan has been approved and you're eager to move into your new home. But before you get the key, there's one more step--the closing.

Also called the settlement, the closing is the process of passing ownership of property from seller to buyer. And it can be bewildering. As a buyer, you will sign what seems like endless piles of documents and will have to present a sizeable check for the down payment and various closing costs. It's the fees associated with the closing that many times remains a mystery to many buyers who may simply hand over thousands of dollars without really knowing what they are paying for.

As a responsible buyer, you should be familiar with these costs that are both mortgage-related and government imposed. Although many of the fees may vary by locality, here are some common fees:

This fee pays for the appraisal of the property. You may already have paid this fee at the beginning of your loan application process.

This fee covers the cost of the credit report requested by the lender. This too may already have been paid when you applied for your loan.

This fee covers the lender's loan-processing costs. The fee is typically one percent of the total mortgage.

You will pay this one-time charge if you have chosen to pay points to lower your interest rate. Each point you purchase equals one percent of the total loan.

These fees generally include costs for the title search, title examination, title insurance, document preparation and other miscellaneous title fees.

If you buy a home with a low down payment, a lender usually requires that you pay a fee for mortgage insurance. This fee protects the lender against loss due to foreclosure. Once a new owner has 20 percent equity in their home, however, he or she can normally apply to eliminate this insurance.

This fee covers the interest payment from the date you purchases the home to the date of your first mortgage payment. Generally, if you buy a home early in the month, the prepaid interest fee will be substantially higher than if you buy it towards the end of the month.

In locations where escrow accounts are common, a mortgage lender will usually start an account that holds funds for future annual property taxes and home insurance. At least one year advance plus two months worth of homeowner's insurance premium will be collected. In addition, taxes equal approximately to two months in excess of the number of months that have elapsed in the year are paid at closing. (If six months have passed, eight months of taxes will be collected.)

This expense is charged by most states for recording the purchase documents and transferring ownership of the property.

Make sure you consult a real estate professional in your area to find out which fees--and how much--you will be expected to pay during the closing of you prospective home. Keep in mind that you can negotiate these costs with the seller during the offering stage. In some instances, the seller might even agree to pay all of the settlement costs.

Escrow: Now What?

Congratulations, you are on your way to owning your very own home! Follow these suggestions (and the advice of your Realtors ®) so that escrow and settlement with go as smooth as possible.

You will be asked for a down payment on the home you are purchasing. You can choose to put down as much or as little as you want (depending on your mortgage), but remember, the more you put down toward the total price of your home, the less time it will take you to pay off and the less your mortgage payments will be every month.

During this period of purchasing your home, you are going to need an escrow or settlement company to act as an independent third party so that you know when and who to give your money to get the deed to your new home. The escrow or settlement company will hold your deposit and coordinate much of the activity that goes on during the escrow period. This deposit check may also be held by an attorney or in the broker's trust account. Make sure that there are sufficient funds in your account to cover this check.

The deposit check will be cashed. Assuming the sale goes through, this money will be applied to the purchase price of the home. If for any reason the sale is not consummated, you may be entitled to receive all of your deposit back, less standard cancellation fees. In certain instances, the seller may be able to retain this money as liquidated damages. Prior to executing a purchase contract, it would be wise to speak with your counsel regarding whether or not it is your best interest to have a liquidated damages clause as part of the contract.

During this time, each item specified in the contract must be completed satisfactorily. By the time you have opened escrow, you have come to an agreement with the seller on the closing date and the contingencies. Each contract is different, but most include the following: 1. Inspection contingency: this should be completed as soon as possible after the contract to purchase is signed as unsatisfactory results of the inspection may mean that you will want to cancel the contract.

Once the contract is signed, you have a period of time to secure funding. If, for any reason, you are unable to secure funding during the period of time granted to you by the contract (and the seller will not provide a written extension of time), you must decide whether you want to remove the contingency and take your chances on getting a loan. You may choose to cancel the purchase contract.

With an attorney or title officer, review the title report. The title must be "clear" to ensure that you do not have legal issues regarding your ownership. Check into local and state ordinances regarding property transfer and make sure that you and/or the seller have complied with them.

This will probably be required before you can close the sale. Due to such requirements as special fire and earthquake insurance, obtaining this insurance may require a lengthy period of time. It would be in your best interest to apply for insurance as soon as possible after the contract is signed.

to schedule to have service turned on when you close escrow.

At this time, you should make sure that the property is exactly as the contract says it should be. What you thought to be a "permanently attached" chandelier that would come with the property might have been removed by the seller and replaced with a different fixture entirely.

You've made it! Once the sale has closed, you're the proud owner of a new home. Congratulations!

All applications are subject to credit approval. Program terms and conditions are subject to change without notice. Some products may not be available in all states. By refinancing an existing loan, the total finance charges may be higher over the life of the loan. Other restrictions and limitations may apply. | This is not a commitment to lend - Envoy Mortgage, Ltd. #6666 (www.nmlsconsumeraccess.org) 10496 Katy Freeway, Suite 250, Houston, TX 77043, 877-232-2461 - www.envoymortgage.com. | Doing business in New Hampshire as Envoy Mortgage Limited Partnership. For other authorized trade names and licenses held see: www.envoymortgage.com/licensing-legal-information/. This is to give you notice that Envoy Mortgage, Ltd. has a business relationship with Place, Inc. and its affiliated real estate agent operators. You are NOT required to use Envoy Mortgage as a condition for purchase, sale, or refinance of the subject property. THERE ARE FREQUENTLY OTHER SETTLEMENT SERVICE PROVIDERS AVAILABLE WITH SIMILAR SERVICES. YOU ARE FREE TO SHOP AROUND TO DETERMINE THAT YOU ARE RECEIVING THE BEST SERVICES AND THE BEST RATE FOR THOSE SERVICES.

Your profile is almost complete! Just a few more details from you.

By digitally signing this form you are providing with your express written consent to send you marketing communications via email and by SMS, calls or prerecorded messages dialed by a natural person or by an automatic or automated telephone dialing system. This express written consent applies to each such email address or telephone number that you provide to us now or in the future and permits such communication regardless of their purpose.By checking the box, you consent to receive marketing text messages. If checked, you consent to receiving texts including marketing and promotional communications, from . Messages and data rates may apply. Message frequency varies. To opt out of text messages, reply STOP. Your consent is not required as a condition of any purchase. By continuing, you also agree to our Terms & Conditions and Privacy Policy

By digitally signing this form you are providing with your express written consent to send you business and marketing communications via email and by calls or prerecorded messages dialed by a natural person or by an automatic or automated telephone dialing system. This express written consent applies to each such email address or telephone number that you provide to us now or in the future and permits such communication regardless of their purpose.

If checked, you consent to receiving texts including marketing and promotional communications, from . Messages and data rates may apply. Message frequency varies. To opt out of text messages, reply STOP. Your consent is not required as a condition of any purchase. By continuing, you also agree to our Terms & Conditions and Privacy Policy

Are you buying or selling a home?

Buying

Selling

Both

When are you planning on buying a new home?

1-3 Mo

3-6 Mo

6+ Mo

Are you pre-approved for a mortgage?

Yes

No

Using Cash

Would you like to schedule a consultation now?

Yes

No

When would you like us to call?

Thanks! We’ll give you a call as soon as possible.

When are you planning on selling your home?

1-3 Mo

3-6 Mo

6+ Mo

Would you like to schedule a consultation or see your home value?

Schedule Consultation

My Home Value

Please confirm your property details:

Sorry, we couldn’t find ''

Please check the spelling, try clearing the search box, or try reformatting to match these examples:

Address: '123 Main St, Anytown' Neighborhood: 'Downtown' Zip: '98115' City: 'Anytown' or 'Anytown, State/Province' MLS number: 'MLS# 38065544'